|

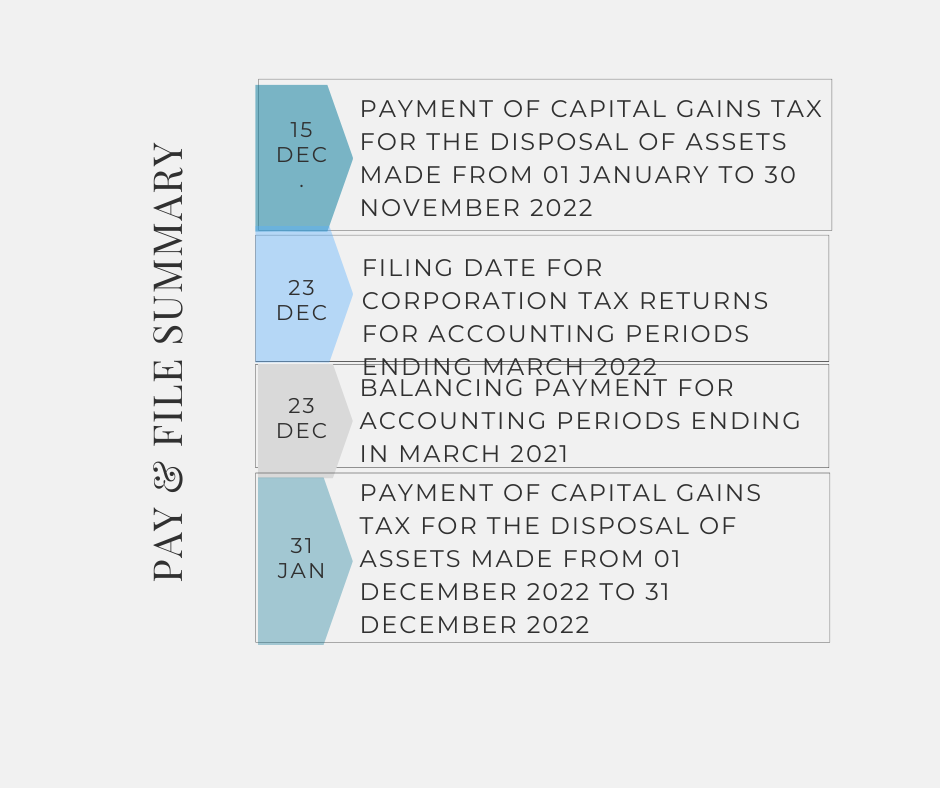

The following is a summary of upcoming pay and file dates:

0 Comments

If your business if affected by these changes – talk to us today On 1 July 2021, the VAT rules on cross-border-business-to-consumer (B2C) e-commerce activities changed. The rationale for these changes is to overcome barriers to cross-border online sales and address challenges arising from the VAT regimes for distance sales of goods and for the importation of low value consignments. It is envisaged that EU Businesses will be able to grow in a simplified, fairer environment within the European Digital Single Market.

The Revenue have confirmed that employers will not be able to back date a registration for the new Employee Wage Subsidy Scheme (EWSS). However an employer can register for the scheme at any stage once they meet the criteria, even if this is after the September payroll is run. Once registered you will only receive the subsidy for all future payroll runs.

As part of the Government’s July Jobs Stimulus, the standard VAT rate of 23% will be temporarily reduced to 21%. This will come into effect from the 1st September 2020 and stay in place until the end of February 2021.

The Revenue have a guide on how businesses should deal with VAT rate changes, which you can find here. One thing to highlight from the guide is if you are sending an invoice to a VAT registered business the VAT rate that should be applied is the rate in force at the time of issue of the invoice. If you are sending an invoice to a non-VAT registered person the VAT rate applied on the invoice will be based on the date the goods or services were supplied, not the date of the invoice. From an accounting point of view most systems should be able to deal with a new rate of VAT. I would suggest adding a new VAT rate as you will need to revert to the 23% from the 1st March 2021. For businesses who pay VAT on a receipts basis you will need to make sure your systems are tracing the VAT back to the invoice and not the date of the lodgement. |

Archives

June 2023

Categories

All

|

RSS Feed

RSS Feed

We create custom business to business strategies. |

SITE MAP |

CONTACT DETAILS |

|