|

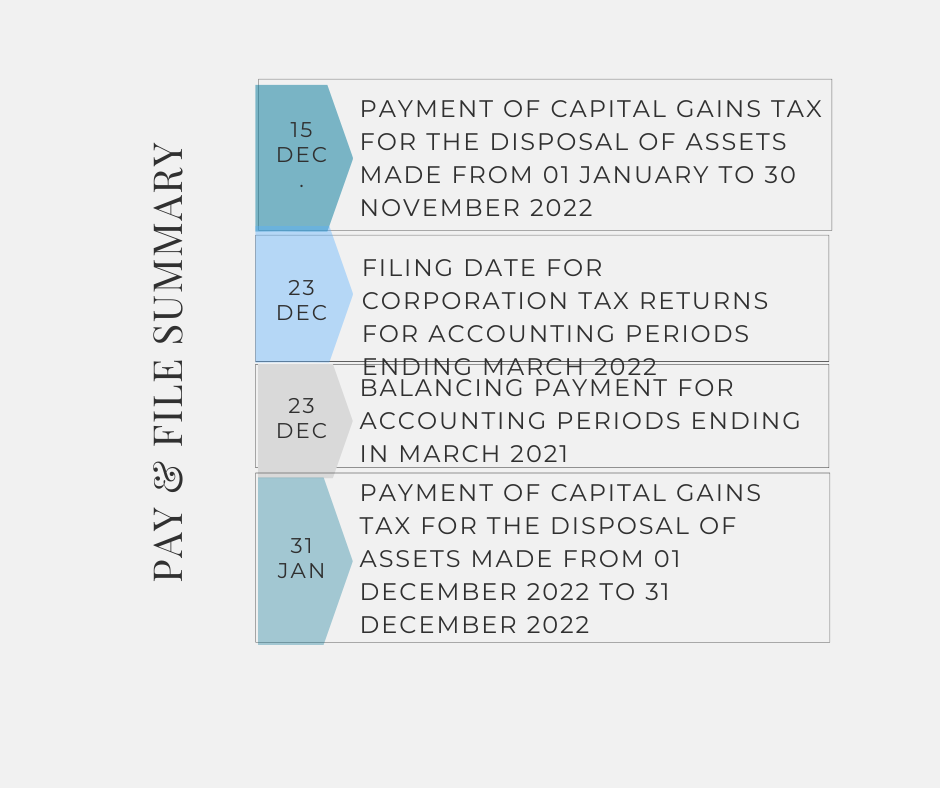

The following is a summary of upcoming pay and file dates:  Revenue has introduced concessions for income tax & corporation tax for employees of Ukrainian employers required to work from Ireland because of the ongoing war in Ukraine for the 2022 tax year. Irish-based employees of Ukrainian employers will not be liable to Irish income tax & USC on Ukrainian employment income that is attributable to the performance of duties in Ireland. The Ukrainian employers will not be required to operate the PAYE system on such employment income. The concession relates solely to employment income that is paid to the Irish-based employees by their Ukrainian employer.

The concessionary treatment will apply for the tax year 2022 where:

The corporation tax concession will disregard the presence of employees, directors, service providers and agents who have come to Ireland because of the war. Revenue may request documentary evidence relating to the reallocation of the individual to Ireland, e.g. a record of the arrival dates to Ireland. EII is a tax relief which encourages individuals to provide equity based finance to trading companies by allowing individuals to obtain Income Tax relief on investments for shares in certain qualifying companies. Since October 2019 the tax relief of up to 40% of the investment made is available in full in the year of investment.

An individual who has made a qualifying investment on or after 1 January 2020 can claim relief on investments up to a maximum of €250,000 per year of assessment. Please note that shares must be retained for at least 4 years. Alternatively, an individual who has made a qualifying investment on or after 1 January 2020 can claim relief on investments up to a maximum of €500,000 per year of assessment subject to the following:

Where an investor invests an amount greater than the maximum amount allowed in a year, the excess over the maximum amount can be carried forward against future Income Tax liabilities. A Statement of Qualification (SOQ) must be issued by the qualifying company within 4 months after the end of the year in which shares are issued. Finance Act 2021 extended this relief by a further 3 years to 31 December 2024.

If your business if affected by these changes – talk to us today |

Archives

June 2023

Categories

All

|

-

Business to Business

Providing Step by Step Guidance

Get in touch for your free consulation today

Contact Us -

-

Over 30 Years Experience

Insight into all aspects and types of business

Get in touch for your free consulation today

Contact Us

RSS Feed

RSS Feed

We create custom business to business strategies. |

SITE MAP |

CONTACT DETAILS

|

|

©

2024 Ryan & Crowley Chartered Accountants